Special Situation: Epsilon Net

Join the resistance?

This thesis is not buying or selling advice. It is for educational purposes only. I own shares of this company.

Epsilon Net is well known within the financial community and therefore I am not going to develop a typical investment thesis. For those who want to familiarize themselves with the company, I am going to recommend some entries that I find of great value:

This investment went from being an error of omission to one of my main positions in my portfolio. I started a position in it (after seeing it go up and up) on September 21, 2023. It was a moment of great commotion in which the stock went from €12 to €7 due to a statement admitting an accounting error which affected the profits of the previous year.

My average purchase price was around €9.5. Of course, I would have liked to buy lower, but I saw so clearly that what happened was a specific problem that did not affect the intrinsic business at all, that I acted quickly. It is these types of situations that I like the most, specific problems that do not affect the fundamentals.

If I bought at a price somewhat adjusted to its fair value, it is because I have always wanted to have Epsilon for many years since I was clear about the sustainable growth in value but the multiple scared me.

Tender Offer

One of the problems of having an aligned board of directors that is strongly committed to your business is that they can reach the point of trying to take it away from you.

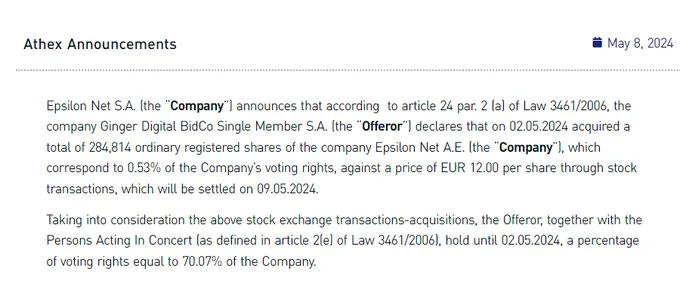

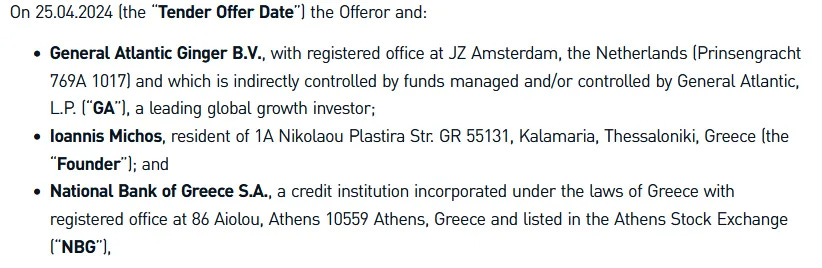

On April 25, Epsilon's trading was halted; a group of investors had launched a tender offer at €12 per share. The group of investors is made up of the current CEO, the Greek national bank and the Ginger investment group, the latter did not own shares although it has been buying since then.

For the tender offer to become a reality, they must obtain 90% of votes in favor. On the day of the announcement, the group's total contribution represented 62.92% of Epsilon's total shares. On the day I write this post, May 23, they control 77.20%, still far from 90% since no one but them is going to vote in favor.

Why does an opportunity arise for the minority investor?

The vote should not extend more than a month from the announcement, although I do not have the precise date. All the investors willing to sell at €12 have already done so, why would they wait if they could sell right away?…

Increasing position now to €12 or starting it can produce 3 scenarios:

1. They manage to privatize Epsilon at €12

The sale would be made effective at €12 and the price would drop somewhat. If the reader is familiar with this type of operation, they will know that there is no fixed percentage but it is usually a 3%-10% drop compared to the agreed price depending on the immediacy of the transaction and whether problems may arise that prevent the operation.

In this case, to simplify it, I would estimate a possible loss of 5% of the investment at €12. For me, this is the worst outcome.

2.1. They fail to privatize Epsilon at €12 and launch a second offer

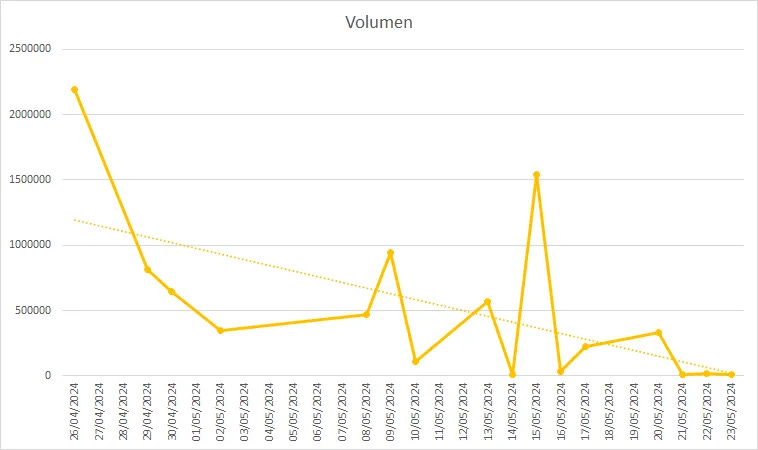

From my point of view, this is the most likely case. The trading volume has decreased to the point of being ridiculous and therefore, they are not going to get 90% of the votes.

If they really want to acquire the entire company, they will launch a second offer higher than the current one. It must be a more attractive price to at least reactivate the volume of the most indecisive and doubtful and be able to buy the shares from them to reach 90%. I estimate €15 as that price, a 25% premium compared to the current one.

Although it is a somewhat fair price and I would be sad to part with this company, it is a quick profit and for which I have seen an opportunity and increased my position. However, there is one more scenario.

2.2. They fail to privatize Epsilon at €12 and nothing else happens

In the short term, the price will suffer somewhat, but if you think carefully... not much. These types of situations create a floor effect in the price, all sellers have already sold and only strong hands remain. I don't think it is the worst scenario since we will enjoy the company in the coming years, which will surely be good, although those who enter now looking only for short-term performance would be disappointed.

That was all, I hope it was an enjoyable read, it is an interesting situation even if you are not an Epsilon investor. If you liked it, please consider sharing the post, and if you are already one of the resistance, share it without fail!