Innoscripta: A GARP Digital Monopoly in the R&D Niche

Business management software with a P/E ~13x growing at +50%

There are other posts about this company online. I haven’t had access to the content behind the paywall. Neither this post nor any other in this substack constitutes a buy or sell recommendation.

Summary

Innoscripta SE is a SaaS software provider (Clusterix) that optimizes the management and application process for R&D tax incentives. With over 2,500 clients, its model is based on success fees and is distinguished by its automated compliance and high technological scalability.

Financial Metrics:

Growth: Accelerated organic expansion, with an adjusted EBIT CAGR of 90.5% (2022-2025) and a minimum revenue projection of €140 million by 2026.

Profitability: High operational efficiency thanks to its SaaS model, achieving an EBIT margin of 67.7% in Q1 2026.

Financial strength: Strong cash generation and no dependence on long-term debt, with a cash position significantly higher than its bank liabilities.

Shareholder return: High free cash flow conversion capacity, supporting a dividend of €4.00 per share by 2025.

Innoscripta can be defined as a “niche monopoly” due to the barriers that protect its dominant position in the R&D incentive management market:

Unique Category: It is the only all-in-one platform that digitizes and automates a sector that previously operated using manual methods or traditional consulting.

Legal Certainty: More than just software, it offers an auditable registration system that guarantees regulatory compliance (Frascati Manual) with the authorities, minimizing legal risks.

High Switching Costs: The deep integration of its platform into companies’ operational processes generates extremely high retention rates (churn <2%), ensuring long-term customer loyalty.

Defensive Advantage Against AI: Its position as a certified registration system and its own AI integration act as a moat against technological competitors, since a generic model cannot offer the institutional and legal validity that the sector demands.

The company’s strategy involves scaling its business and increasing its product portfolio:

Global Expansion: Strategic entry into the US, France, and UK in 2026 to significantly expand its total market reach (TAM).

Regulatory Boost: New regulations in Germany (increased tax base and fixed deductions of 20%) that stimulate local demand.

Efficiency and Valuation: The relocation of the headquarters improves governance and margins, supported by analysts who maintain a “Buy” recommendation with a target price of €225.

Valuation: Trading at EUR 76 per share (equivalent to an Enterprise Value (EV) of ~EUR 700 million) and taking into account the management’s projection of at least EUR 80 million of EBIT by 2026, Innoscripta is currently trading at a P/E of ~13x.

For a platform boasting year-over-year revenue growth of nearly 60% with industry-leading operating margins, is this company undervalued compared to other high-growth B2B SaaS leaders?

Throughout this post, we’ll break down why I currently consider the company cheap, whether its growth is sustainable and what strategy the company has to further accelerate it, the potential impact of its risks, and how to be ahead of the curve if growth will slow, so we don’t get caught out.

Company activities

What Innoscripta does is essentially digitize all the bureaucratic paperwork surrounding public funding and tax breaks for R&D.

Instead of companies wasting weeks on spreadsheets and emails managing research projects, Innoscripta integrates all of that into its platform, Clusterix. Its main function is:

Centralize management

Ensure legal compliance

Process incentives: Ultimately, their job is to guarantee that their clients actually receive the money from subsidies or deductions. In fact, they only get paid if the client receives the subsidy.

Adapt quickly to new markets: Thanks to their technology, if a country changes its laws or a company starts operating in a new territory, they can adjust their software to comply with those local regulations in a matter of weeks.

Basically, they function as a legal and administrative “shield” that is responsible for converting the technical work of a company into an impeccable file for the public administration.

Tailwinds in the sector

Innoscripta operates at the intersection of technology and fiscal policy, a strategic niche fueled by the global commitment of governments to funding private innovation. While governments compete to attract talent through generous subsidies and tax breaks, accessing these funds is a bureaucratic, technical, and legal labyrinth; companies don’t need just another software solution, but rather absolute protection against future audits.

Historically, this market was dominated by slower and more expensive traditional consulting firms. Innoscripta has transformed this artisanal service into a scalable SaaS product. Far from being a risk, its reliance on regulations has become its greatest strength: in the face of the geopolitical race for technological competitiveness, governments not only maintain but also expand these subsidies, positioning Innoscripta as a key player in ensuring the flow of public funds to the business sector.

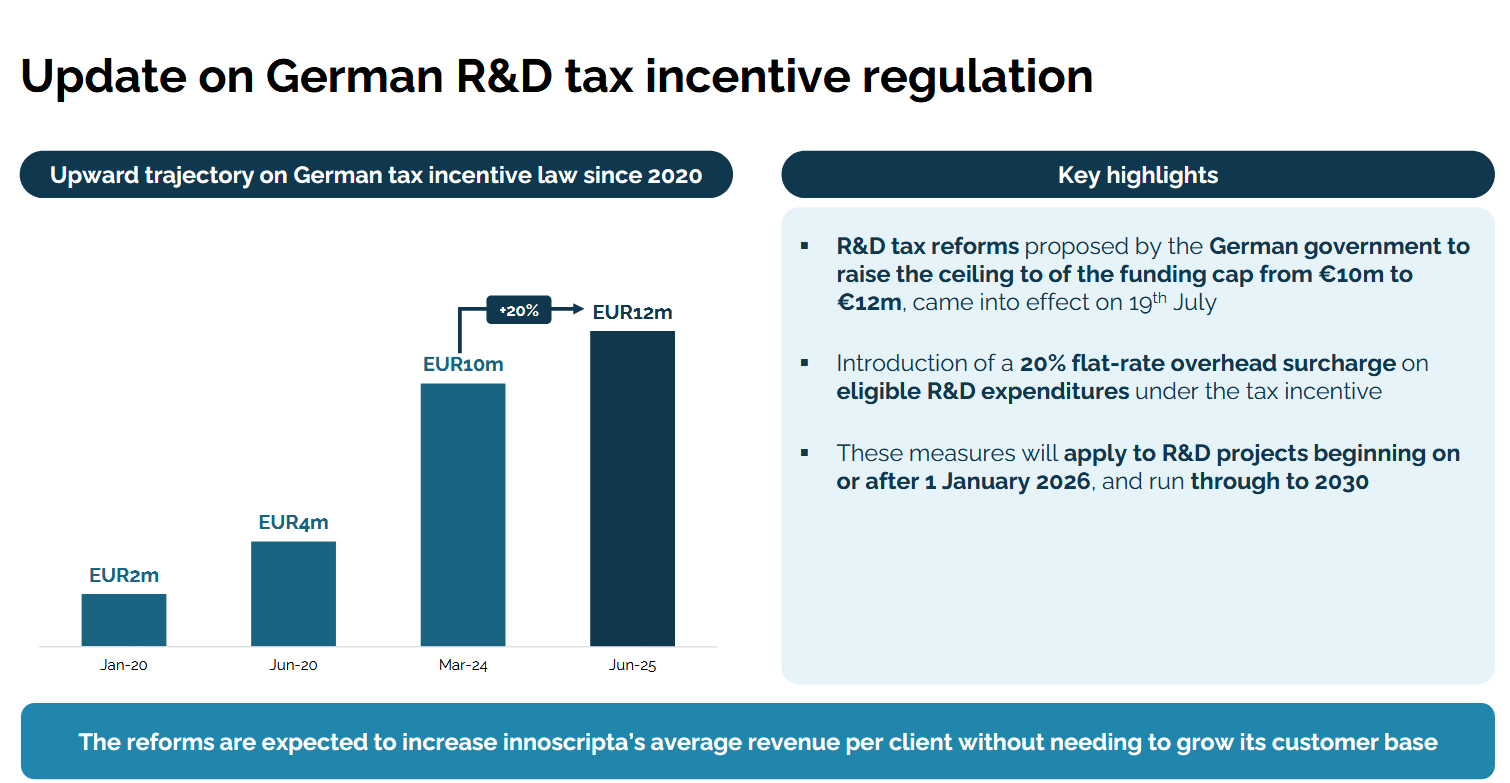

Germany’s R&D incentive policy, currently Innoscripta’s main market, has been undergoing a period of consolidated structural expansion since early 2026. The government recently raised the ceiling for eligible expenditures from €10 million to €12 million per project, making it easier for companies to declare larger investments. This measure is complemented by the introduction of a 20% flat-rate deduction for overhead costs, which significantly simplifies the administrative burden and makes the tax return much more predictable.

Far from being subject to the fluctuations of a specific election cycle, these incentives reflect a long-term state strategy. There is a solid, cross-party political consensus aimed at safeguarding German industrial competitiveness against pressure from China and the United States. In this context, the government’s roadmap prioritizes simplifying and accelerating R&D processes, consolidating an environment where this support is not only maintained but strengthened as a critical pillar for the technological transition, thus guaranteeing the strategic relevance of platforms like Clusterix.

In their H1 2025 presentation (their first business presentation), they show some data on what we can expect from the sector:

This slide conveyed two powerful messages:

The current measures will remain in effect until 2030; there will be no legislative changes.

Each time the financing limit is increased, each existing customer will be able to spend more. This is an optional lever for organic growth.

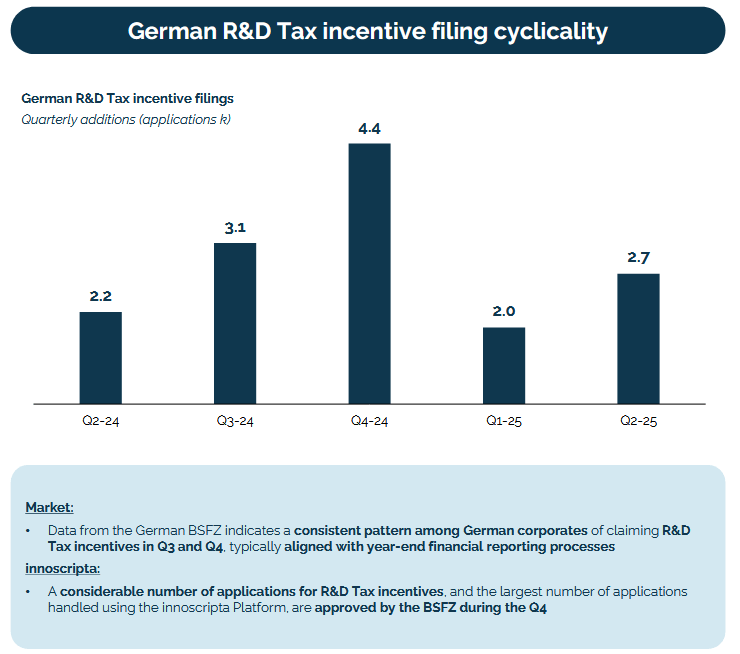

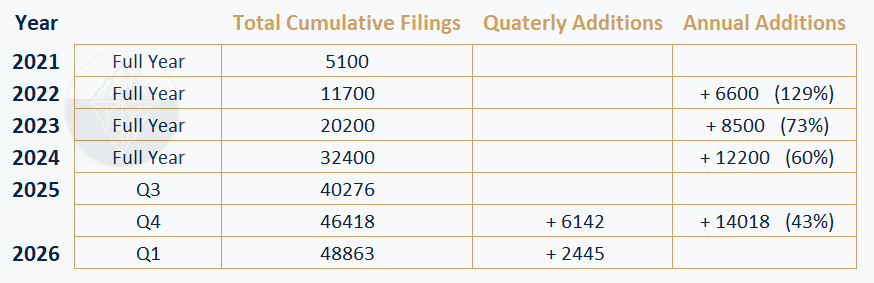

Overall, the management team is very optimistic about this, but it’s always wise to verify all the information provided. In that same presentation, they also communicated the number of applications received and the seasonality involved.

The sector is experiencing a boom in proposals, which is driving this company’s very high growth. To know before anyone else when this growth will slow, one can track the public proposals companies submit for subsidies. It’s not accurate to assume this level of growth is sustainable in the German market; however, it’s clear that it’s currently growing at a good pace. By examining public data, one can “predict” future growth.

Looking at this data, we must not forget that this is simply the growth of the target market; at the end of 2025 the company had 2500 clients in this market.

Company strategy

In the medium term, Innoscripta’s strategy revolves around aggressive geographic expansion and a deeper focus on the large accounts segment, all supported by an increasingly efficient cost structure. Their plan does not aim to diversify products, but rather to scale their successful model into new markets that share similar regulatory frameworks and are highly lucrative.

This international expansion is supported by its technological advantage: thanks to a no-code architecture, they can adapt the platform to a new country’s regulations in just two weeks. After consolidating its position in Germany, the company opened sales offices in the United States and France this year, with the United Kingdom as its next target. This entry into large markets aims to maximize its market share in ecosystems where investment in innovation is constant, allowing them to absorb R&D budgets on a global scale.

At the same time, the company is successfully executing a “Land & Expand” strategy with large conglomerates. The case of DANAHER, where the initial implementation in a subsidiary (Leica Biosystems) triggered adoption across the entire group, serves as a roadmap: once the software is integrated into the daily operations of a large corporation, the technical dependence and switching costs ensure a highly predictable long-term relationship.

Finally, this growth is accompanied by a leap in operational efficiency following the recent relocation of its headquarters to Tutzing. This move is not only logistical, but a pillar of its financial strategy, since by optimizing governance and sustainably reducing operating costs, the company is achieving a direct increase in its net profits (5-7M of additional profit).

Competitive Advantages

Looking through the published material, these are the competitive advantages I see in this business:

A difficult-to-copy institutional moat: Innoscripta doesn’t just sell software, but a layer of legal security. By acting as the official “system of record,” its platform guarantees automatic compliance with complex regulations (such as the Frascati Manual), something no generic AI or new competitor can offer without years of experience and established trust with tax authorities.

Switching costs that protect the client: Once the tool is integrated into the daily workflows of a large corporation’s technical and financial departments, operational dependence becomes total. This is the real reason why its churn rate is less than 2%: switching providers would entail an audit risk and administrative paralysis that no company is willing to take.

An expanding unfair advantage (no-code architecture): While any competitor would need months of development to adapt its system to the tax laws of a new country, Innoscripta’s technology does it in just two weeks. This agility is what allows them to enter new markets (US, France, UK) with a speed that simply leaves the rest of the market behind.

Corporate network effect (Land & Expand): Their strategy of entering large multinational groups through a single subsidiary is a goldmine. When one division demonstrates that subsidies flow smoothly, adoption by the rest of the group is natural, rapid, and requires minimal sales effort, which dramatically increases profitability per customer.

Margins worthy of a monopoly: Thanks to their SaaS model, they have achieved operational leverage that few companies possess. Since they don’t need cumbersome physical structures or armies of salespeople to scale, revenue growth translates directly into EBIT margins that are already approaching 70%, making each new customer significantly more profitable than the last.

Competitors

To understand Innoscripta’s true competition, you have to look beyond other management software. In reality, its “competitor” isn’t another technology company, but rather corporate inertia.

These are the three real alternatives companies face today, and why Innoscripta usually wins out:

1. The “Do It Yourself” model (Excel and administrative chaos)

This is the most common and dangerous competitor: the spreadsheet. Many companies, especially medium-sized ones, try to manage their R&D incentives internally using Excel, interdepartmental emails, and manual time tracking.

Why companies choose it: They think it’s “free” because they don’t pay a subscription.

Why Innoscripta wins: The hidden cost is extremely high. Manual management is slow, prone to human error, and, above all, doesn’t generate a solid audit trail. When the tax authorities come looking for answers, the disorganization of Excel becomes a serious tax risk. Innoscripta offers centralized control and traceability.

2. Traditional consulting firms (“Big Four” and specialized boutiques)

Historically, if a company wanted to process R&D deductions, it hired a consulting firm. These firms assign experts to review the projects, write the technical report and present the documentation.

Why companies choose it: Because of the personal treatment and the perception of security. They feel that if there is a problem, they have a natural person behind them.

Why Innoscripta wins: The consulting model is artisanal, expensive and, above all, does not scale. Innoscripta offers an all-in-one solution that is significantly cheaper, much faster and that allows the company to have real-time control, instead of depending on the consultant on duty sending them a report once a year. In addition, consulting cannot offer the full integration with HR and finance systems that software like Clusterix provides.

3. Niche solutions or “Point Solutions”

There are small software solutions that help control time tracking or manage projects, but these are isolated tools that don’t address the tax implications.

Why companies choose them: They are inexpensive and easy to implement for a specific department (for example, development).

Why Innoscripta wins: This is where the “integration” moat shines. These tools don’t communicate with the tax authorities; they are simply time clocks. Innoscripta not only measures time but also translates it into the legal language of the OECD. A company may have time tracking software, but if that software doesn’t guarantee tax subsidies and tax validity, it will ultimately need something like Innoscripta to complete the process.

4. What about AI?

AI has no civil liability. If a company uses a generic AI and makes a mistake in its justification, the company bears 100% of the responsibility to the tax authorities.

Furthermore, Innoscripta is a software company that uses AI, not a company that competes against AI. Their advantage is that they have turned AI into an operational advantage for themselves, while maintaining the “barrier to entry” of legal trust, preventing generic models from entering the market.

The Challenge

If Innoscripta can convince that executive that their “opportunity cost” (the money lost due to errors in applications or the time spent by staff on bureaucratic tasks) is much greater than the price of their subscription, the sale is done. Their advantage is that, once the client experiences automation and sees the grant money flowing into their account risk-free, going back to Excel or traditional consulting firms becomes virtually impossible.

Ultimately, their real competition is inefficiency, and since inefficiency is expensive and dangerous, Innoscripta has the upper hand.

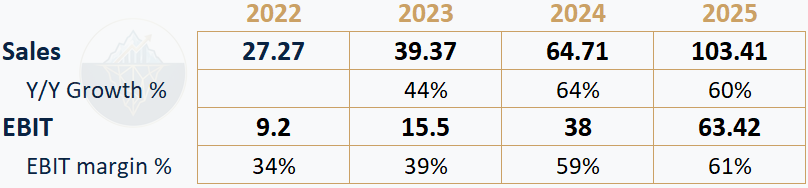

Financial Metrics

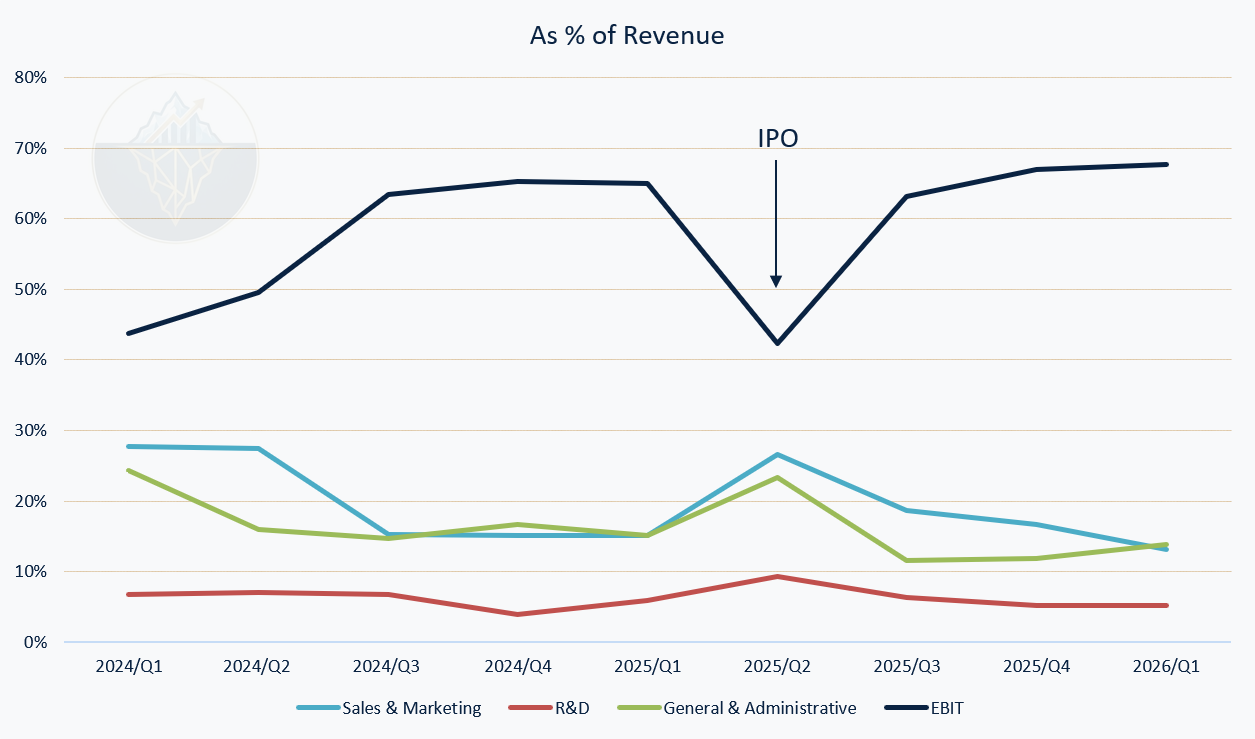

Understanding expenses in this business is straightforward. They report their main expense categories quarterly. We know that the largest expense is sales and marketing; the strategy of internationalizing the business will lead to increased investment in this area. After these three categories, the next largest expense is taxes, consistently representing 33% of EBT.

This chart I’ve prepared clearly shows how the EBIT margin expands thanks to Clusterix’s scalability.

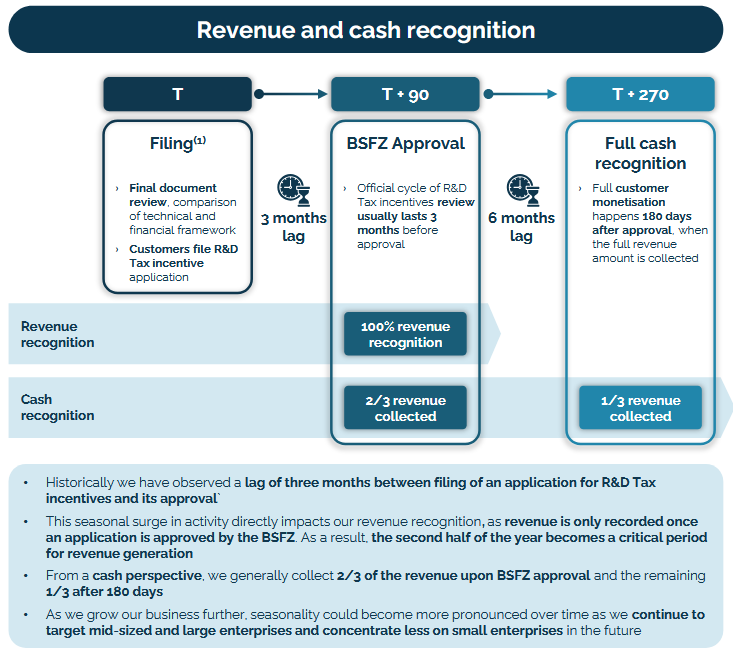

We also have some interesting information regarding cash conversion. The following slide was shown in the H1 2025 presentation:

Management and Capital Allocation

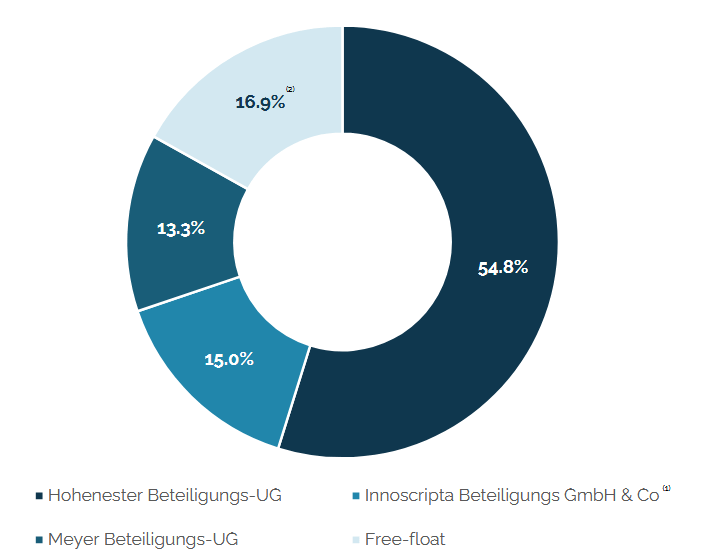

Michael Hohenester is the CEO; there isn’t much information about him online. It’s known that he has been managing the company since 2012. The same is true for the CFO.

I don’t like how little information is available about them, but I’m reassured by the amount of shares they both hold with a lock-up clause until 2028. Furthermore, the fact that they have high-profile clients, ample cash flow, and distribute dividends dispels any suspicion of fraud.

Another thing I don’t like is that during the IPO they took advantage of the opportunity to issue shares at a price of €120, which, in my opinion, is a bit high. I miss having medium- to long-term incentive programs linked to KPIs. Therefore, I don’t see a quality management team running this business.

While I’m not a dividend fan, it’s always appreciated. They declared a dividend of €4 per share for 2025 for each of the 10 million shares. Profit for the year was €42.39 million and free cash flow was approximately €40 million, which makes the calculations easy. International expansion won’t require large investments, so they will likely distribute another dividend next year, which I estimate will be €6 per share.

The company maintains an extremely healthy balance sheet (more than €68 million in cash compared to a debt of barely €50,000). This gives them the option to do so if an inorganic opportunity arises (acquiring a small competitor or complementary technology); they have the cash to do it without diluting the shareholder.

Valuation

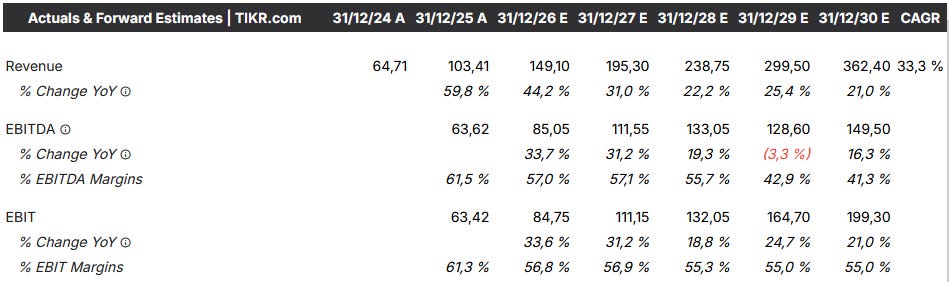

Only two analysts cover the company, and their growth estimates, in my opinion, are overly cautious given how they execute their strategy. In the first quarter, they’ve already reported a 57.5% increase in sales and an EBIT margin of 67.7%. As the quarters progress, it’s likely that analysts’ estimates will be revised upwards, serving as a short-term catalyst to raise the share price.

Furthermore, they expect to incorporate revenue from other countries in the second half of the year, although I find it impossible to predict its impact. Even so, the current growth momentum leads me to believe they’ll have no problem exceeding €90 million in EBIT and a profit of €60 million.

I previously estimated a forward P/E ratio of 13x based on an €80M EBIT for 2026. I believe there are reasons to think this figure is conservative and that there will be no further multiple compression; however, I am not counting on any multiple expansion in my calculation of future returns. As long as growth doesn’t suddenly slow down, Innoscripta could generate returns exceeding 20%, according to its quarterly report.

The €4 dividend gives this stock a dividend yield of ~5%. This is quite reasonable for a company currently growing at 50%.

Risks and Weaknesses of the Thesis - Why are stocks cheap?

If the company is so good, why is it so cheap? The market isn’t stupid, but sometimes it has biases or fears that negatively impact the stock price. We separate real risks from inefficiencies.

Small Cap and Recent IPO

The first obstacle to the stock price is structural: Innoscripta is a small-cap company with a very recent IPO (Q2 2025). Large institutional funds (those that truly drive a stock’s price) typically have strict mandates prohibiting them from investing in companies below a certain market capitalization or without a publicly available track record of at least three to five years. Because it has been listed for such a short time, the market still views it as being in a “proof” phase. Investors prefer to wait and see if the results of the coming quarters are consistent before assigning a valuation multiple, which keeps the stock trading at a discount due to its illiquidity and youth.

Opportunity

The Specter of the SaaSpocalypse

The market has severely punished any software company whose business seems easily replaceable by AI agents. There is a widespread fear that generative AI (LLMs) will turn the writing of technical reports into a free commodity, destroying industry margins. Although we have seen that Innoscripta’s real advantage lies in legal certainty, the traceability of audits, and its “System of Record” status (something AI cannot certify), the market tends to shoot first and ask questions later. Until the company demonstrates quarter after quarter that AI is a tool that improves its own margins and not a threat to its revenue, this risk will continue to weigh on its valuation.

Opportunity

Pure SaaS or Consulting in Disguise?

Another reasonable market concern is the quality and recurrence of its revenue. Although marketed as a SaaS with extremely low churn, investors wonder if the revenue is truly recurring (ARR) or if it depends on the lifecycles of its clients’ R&D projects. What happens if a company finishes its major innovation project? Will it continue paying the subscription? If the market perceives the revenue as transactional (paid only when there’s a subsidy) rather than a subscription for essential infrastructure, it will refuse to pay the high multiples typical of cloud software.

Medium Risk

The Danger of Large Clients

The success of the Land & Expand strategy carries a risk of market concentration. Having giants like Danaher deploying the software across all their subsidiaries is excellent for operational profitability, but it worries risk analysts. If a very high percentage of revenue depends on a handful of multinational conglomerates, the loss of a single key client would leave a huge hole in the profit and loss statement that would be very difficult to fill with smaller clients.

Low Risk

The Edge of the Regulatory Sword

This is the ultimate existential risk. The entire business model revolves around political will. Although the outlook in Germany until 2030 is excellent (with a ceiling of €12 million), the regulatory risk is undeniable. If a change of government or a sovereign debt crisis were to force European countries to drastically cut innovation subsidies, Innoscripta’s total addressable market (TAM) would shrink overnight. Investors demand a risk premium (a lower price) to accept this dependence on government funding.

High Risk

The Challenge of International Execution

Ultimately, the market doesn’t guarantee future success. The company has begun its expansion into the United States, France, and the United Kingdom, but success in Germany doesn’t ensure success abroad. Each country has a distinct business culture, entrenched local competitors, and specific regulations. Until Innoscripta demonstrates that its no-code platform truly resonates in these new markets and generates significant revenue outside the German ecosystem (DACH), the market won’t price in that potential growth.

Medium Risk

The Illusion of “Skin in the Game” (Management Risk)

The bullish narrative highlights insider buying, but the math is concerning. During the May 2025 IPO, the company raised zero capital while the founders pocketed nearly €280 million. Although the CEO recently bought back €12 million in stock, this represents less than 5% of their cash-out. This raises a legitimate fear: management has already secured their wealth and might just be paying a "maintenance fee" to support the stock price until their lock-up period expires in May 2028, rather than being truly aligned with minority shareholders. High Risk

Conclusion

Throughout the research process, I’ve concluded that this company doesn’t meet the quality and long-term value requirements I demand of my ideas. The management team is a major drawback that generates distrust among investors. Added to this is the heavy reliance on German subsidiary policies, which raises serious doubts about Innoscripta’s terminal value.

I found Alex’s post very helpful, as he highlights several negative points. I agree with some of them, but not with others. I’m sharing the link.

However, I still see an opportunity to make money in this stock. The growth is there and will continue to push at high rates, with the option of seeing how they scale the business in other countries. If they show solid results, Innoscripta will have the opportunity to build a business less dependent on R&D subsidies.

There are times when the safety margin of an investment is provided by growth; this is one of them.

Today innoscripta announced it's first French customer wins. Very encouraging and a great business with a bright future. Stupidly cheap 👍